What you need to know before it starts on 1 July 2026

What is Division 296?

Division 296 introduces an additional tax on certain superannuation earnings for individuals with large total superannuation balances.

The legislation has passed Parliament, received Royal Assent on 13 March 2026, and applies from 1 July 2026.

Who is affected?

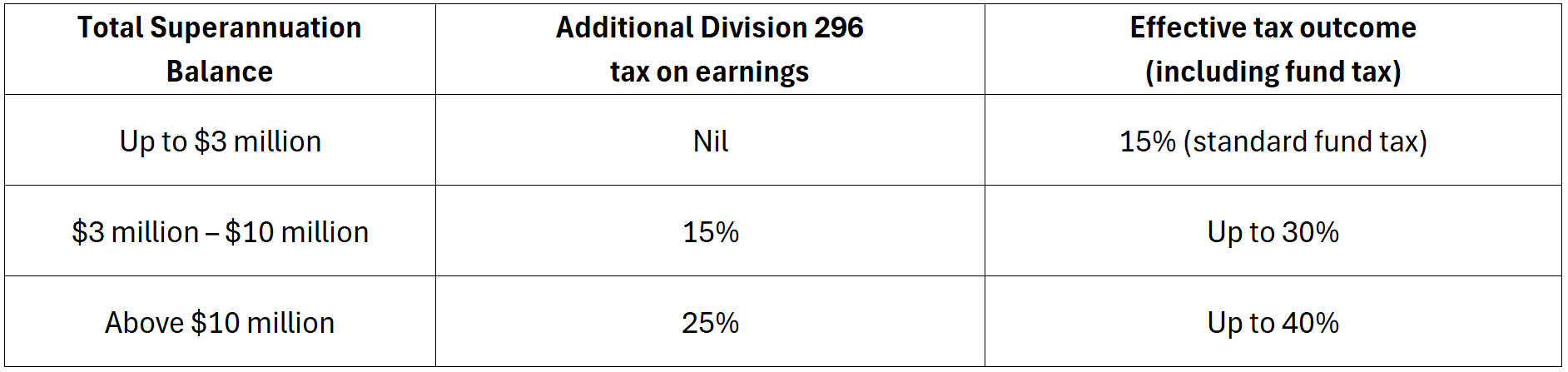

Division 296 applies to individuals (not super funds) whose Total Superannuation Balance (TSB) exceeds $3 million or $10 million.

TSB is measured across all super interests combined, including SMSFs, retail funds and industry funds.

Key thresholds and tax rates

The additional tax applies only to the portion of earnings attributable to balances above each threshold. Both thresholds are indexed to CPI in set increments.

What earnings are taxed?

Division 296 uses a fund-level realised earnings approach. The tax will apply to realised earnings for the 2026–27 year, with assessments issued after 30 June 2027.

Importantly, it was confirmed that unrealised capital gains are now excluded from the calculation.

Earnings are based on normal tax concepts, with adjustments.

Transitional year – how Division 296 applies in 2026–27

For the 2027-28 year onwards, an individual’s Total Super Balance will be assessed at the start and end of the financial year; and the Division 296 tax will be assessed on the higher of the two balances.

However, the 2026–27 year is subject to special transitional rules. For this first year only, an individual’s Total Superannuation Balance is assessed solely at 30 June 2027 (not at both the start and end of the year).

This provides a one-off opportunity for individuals to reduce their TSB before 30 June 2027 if they wish to avoid being subject to Division 296.

Cost base reset – transitional CGT adjustment (SMSFs)

SMSFs may elect a one-off cost base reset for Division 296 purposes at 30 June 2026.

If elected, the cost base of all CGT assets held at that date is reset to their market value for Division 296 calculations only (this includes assets in an unrealised loss position).

This ensures that capital gains accrued before 1 July 2026 are excluded from future Division 296 earnings when assets are sold.

The reset is optional, applies on an all-or-nothing basis to all CGT assets, and is irrevocable once made.

The election must be made by the due date of the SMSF’s 2026–27 annual return.

Importantly, the reset does not alter the cost base for ordinary SMSF income tax or CGT purposes – separate records will be required.

How the tax is assessed and paid

Division 296 tax is assessed to the individual, not the super fund.

Super funds calculate Division 296 earnings and attribute them to affected members.

The ATO issues an assessment to the individual, who may choose to pay personally or release the amount from super, similar to Division 293 tax.

SMSFs – additional considerations

For multi-member SMSFs, Division 296 earnings must be attributed between members, generally requiring an actuarial determination.

Single-member SMSFs are generally excluded from this actuarial requirement.

Why this matters now

With Division 296 now law, affected individuals and trustees should understand whether their super balances may exceed $3 million.

Trustees should plan for valuation, record-keeping, actuarial requirements and potential cash-flow impacts.

While no immediate action is required before 1 July 2026, preparation ahead of the transitional year is critical.

Contact Us

If you think you may be impacted, or you’re simply unsure, we recommend having a conversation sooner rather than later.

Contact our team and we’ll help you understand what this means for you and what steps you should consider next.